From the growth of emerging markets to musical tastes, ahead: what I read on the web this week.

Bonus – Remnants of the IBM PC days

In the category of trivia only, at the bottom of the article at the link above—a link ostensibly about screenshots in Window 10—is Bonus section that talks about the vestigial organs of your windows-machine keyboard. I still remember the feel of the keyboard on the first IBM PC I used in high school. It had three keys on it, which are on the wireless Microsoft keyboard I’m using now. Read this article for more on the purpose of Scroll Lock, Pause/Break (actually, my current keyboard doesn’t have a Break key.)

This is a really cool site, if for no other reason than to show how good design and internet functionality can come together, but I’m nearly certain it’ll have nothing to do with your job. Go to the site, select a year, like my 1987 high school graduation year, and watch the top 100 songs of the year scroll by—top five at a time—with the number one song playing until it gets overtaken by another. Just be sure to be able to do a quick Alt+Tab when the boss walks by. I went to the site because it’s my job to tell you what I checked out this week.

Strong Secular Prospects for Emerging Markets

Now, back to some serious stuff. This piece and accompanying chart that’s posted at The Big Picture blog shows Fidelity’s estimates of growth for emerging markets countries as compared to the developed markets; aka third world versus first world. India, for example, is expected to grow at about 6% annually, for the next twenty years, while Italy, Japan, Spain, Netherlands, and Germany are all expected to grow at less than 1% per year. Aside from the fact that forecasts are almost always wrong, this could lead one to make bad investment decisions, because there tends to be a negative correlation between GDP growth and country stock market returns. The reason for that can be found in a Price:Earnings (P/E) ratio. This chart and its implications only affect the denominator, the E. Of even more importance is the P, or price, or what one has to pay for the investment. I had a friend who once said one could make money on anything…at the right price. Markets with robust anticipated growth get bid up, and their rising valuations squeeze out any extra return. A better approach for investing would be to also chart the P/E ratio before investing, because that will be a far more important determinant.

{kind=link}

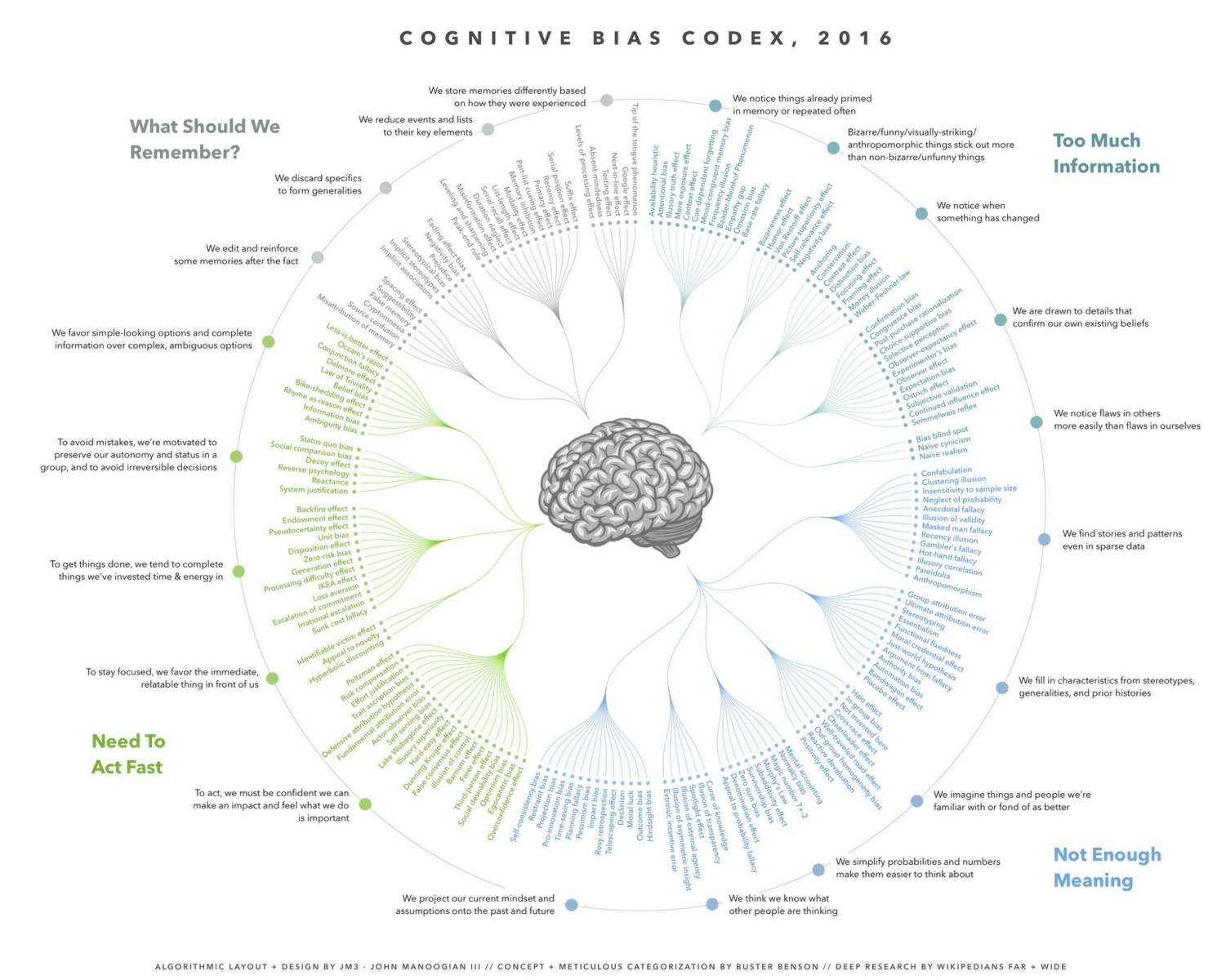

If it weren’t for this being presented in some hippie-flower, lotus-like diagram, this would be dreadful, but it’s a well laid out look at all of the cognitive biases, categorized (e.g. Too Much Information) and sub-categorized (e.g. We are drawn to details that confirm our existing beliefs.) I wouldn’t notice all these flaws in your and my clients’ thinking, if I didn’t exhibit so many of them myself. An example of a cognitive bias is the Recency Illusion, which I can nearly guarantee you suffered from in…oh…February 2009. You thought the market was on its way to a hot place—or Dow 2,500 (same thing). It’s our tendency to take the recent past and project it into the future. This is a delicious piece, with so much to learn. What’s the IKEA effect? I must know.

Rethinking Due Diligence and Manager Selection

Good thing this one is last, as I’m sure I’m going to lose you here, but this is a huge part of what we do, trying to insure that our retirement plan participants have access to a good set of investment choices, along with our individual clients, who are after the same thing. Tom Brakke, CFA, who writes a lot on his blog, The Research Puzzle, about the subjects in the article title, above. This article are excerpts from a Q and A session that followed a presentation he made. In it, he addresses, among others, these questions: If you could only pose one question to an asset manager, what would it be? and “Given the work involved in doing proper due diligence, and given the underperformance of active managers, is it better just to throw in the towel and go passive? I intend to read the full proceedings, which are offered through a link in this piece, as just the couple of Qs and As in the link above are enough to make me want to read more.

Graig P. Stettner, CFA, CMT

Financial Advisor & Partner

Strategence Capital

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

The economic forecasts set forth in the material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Tom Brakke is not affiliated with LPL Financial or Strategence Capital