The Wall Street Journal of July 6 featured an article by respected columnist Greg Ip, titled, “Why Soaring Assets and Low Unemployment Mean It’s Time to Start Worrying.” In it, he suggests that the current economic environment is exhibiting the preconditions for recession: “a labor market at full strength, frothy asset prices, tightening central banks, and a pervasive sense of calm.” He goes on to say that none of these things mean that a recession is imminent, that, in previous periods, some of these conditions were present several years before a recession came. Still, at just two years shy of a record, one wonders if this expansion deserves to be in the record books.

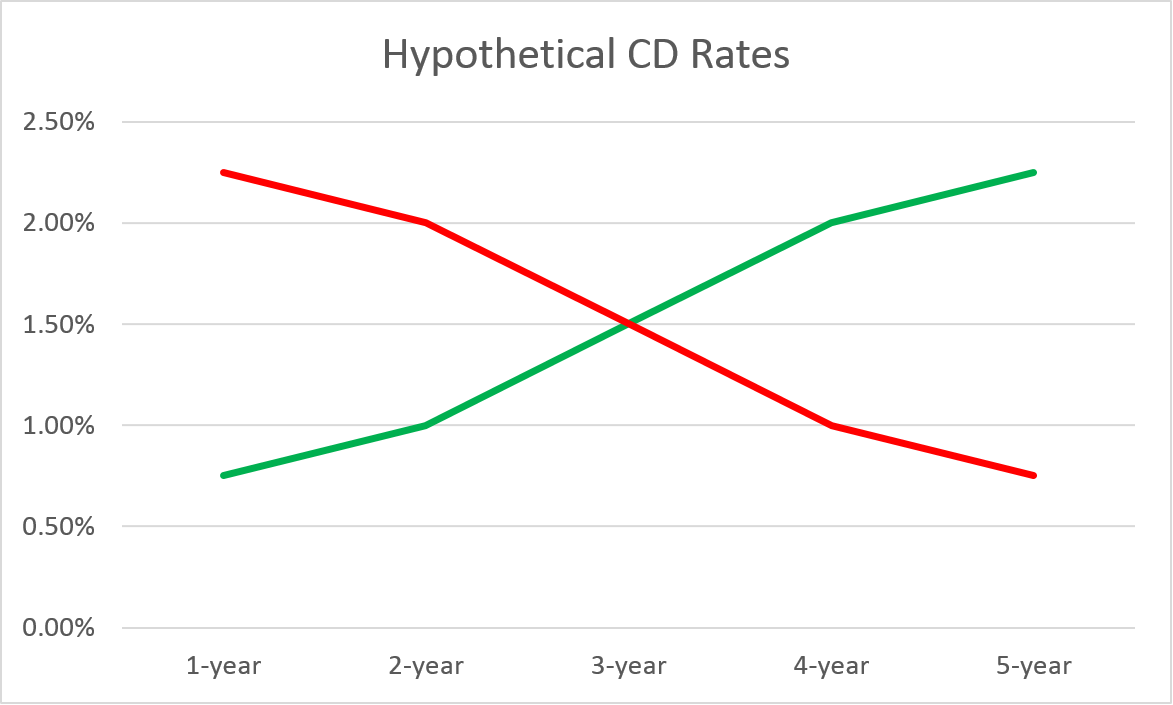

One thing notably absent from the list of things to worry about is an inverted Treasury yield curve. The yield curve is a graphic depiction of the yield available across the maturity spectrum. Imagine your local bank’s certificate of deposits (CD), where the yield is listed fora 6-month CD; a 1-year CD; and so forth. Typically, one expects to see higher yields for longer maturities (green line, below). This is, in part, a compensation for inflation, and this relationship (higher – longer) is considered normal. When the bank starts paying less for longer CDs than it does for shorter CDs (red line, below), you know something is not right. This latter condition is known as an inverted yield curve.

click to enlarge

Just as an inverted yield curve at your bank would be a red flag, so it is with the economy. When yields on bonds issued by the U.S. Treasury are lower on longer-dated securities, then one knows that something is rotten in the state of Denmark.

- An inverted yield curve might indicate a Federal Reserve that is hiking rates aggressively; or

- Since higher yields for longer securities include compensation for inflation, and since inflation is associated with a growing economy, well…you get it.

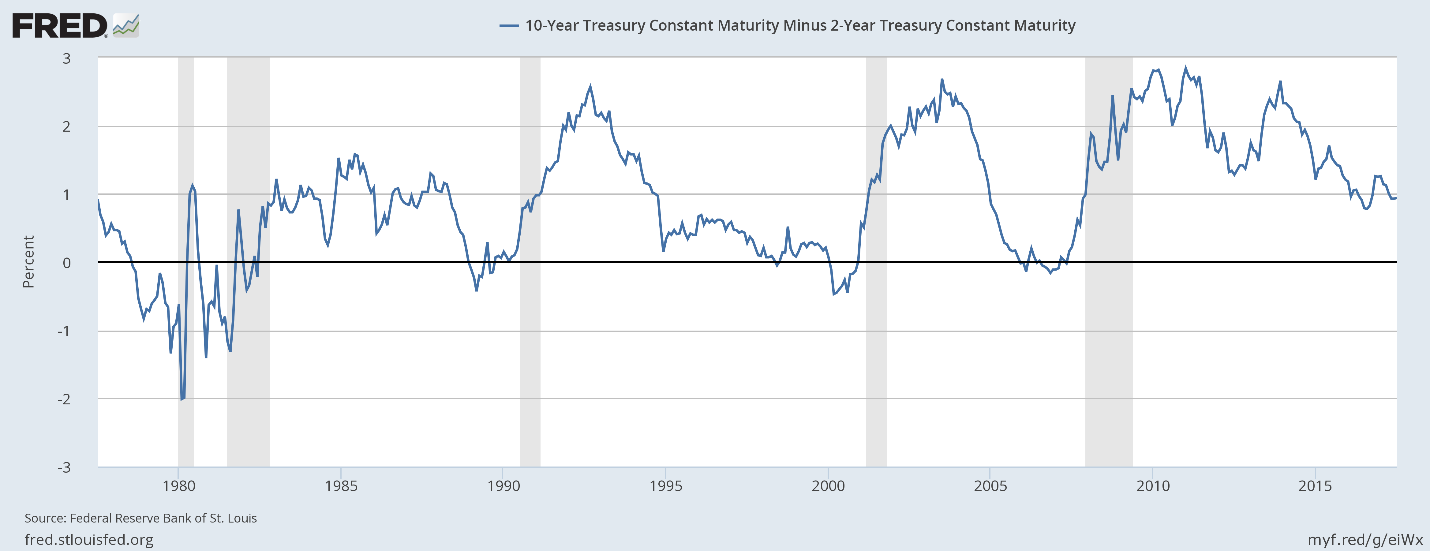

As can be seen below, an inverted yield curve (2-year Treasury yield > 10-year yield) has preceded each of the last five recessions. Importantly, while the trend is from upper left to lower right, the relationship is still decidedly positive.

click to enlarge

While there is always someone who says this time is different, with the yield curve batting 1,000, it deserves a place on the list of things to watch. And, right now, it’s saying recession is not imminent.

Securities offered through LPL Financial, Member FINRA/SIPC. Investment advice offered through ADVISORS PRIDE, a registered investment advisor. ADVISORS PRIDE and Strategence Capital are separate entities from LPL Financial.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. Investing involves risk including loss of principal.